Josh Rauh of the Hoover Institution has a great piece on the threat we face because of rising interest payments on the debt. After making the case that the measure that matters for assessing this threat is the share of revenue consumed by interest payments, he notes that:

Using Table 1-1 from the latest (June 2024) updates to the Budget and Economic Outlook from the Congressional Budget Office (CBO), interest expenditures as a share of federal revenues will be 18.2% this year ($892 billion of interest on $4.890 trillion of revenue) and 20.2% in 2025 ($1.016 trillion of interest on $5.038 trillion of revenue), in the absence of changes to taxes or spending.

History shows that while the 18% threshold was crossed in 1991 . . . we are in uncharted territory crossing the 20% mark. . . .

I have also done a coverage calculation that uses the CBO’s figures and projections but removes in the revenue denominator the tax revenues from the Social Security Old Age and Disability Insurance (OASDI) program. This calculation is relevant under the assumption that these Social Security revenues, which already are insufficient to pay for those programs, are not accessible to pay interest. Under that scaling, the 2024 and 2025 interest-to-revenue ratios rise to 25.1% and 27.9% respectively, relative to the 1991 level of 25.8%.

According to the CBO’s newest report, the deficit in 2024 was $1.8 trillion. That’s a $139 billion increase over last year. (It is also much more than the $905 billion 2024 deficit projected by CBO back in 2021.)

CBO shows that tax receipts were up 11 percent last year, and receipts from the corporate income tax were up 26 percent. Meanwhile, “outlays rose by an estimated $617 billion (or 10 percent).”

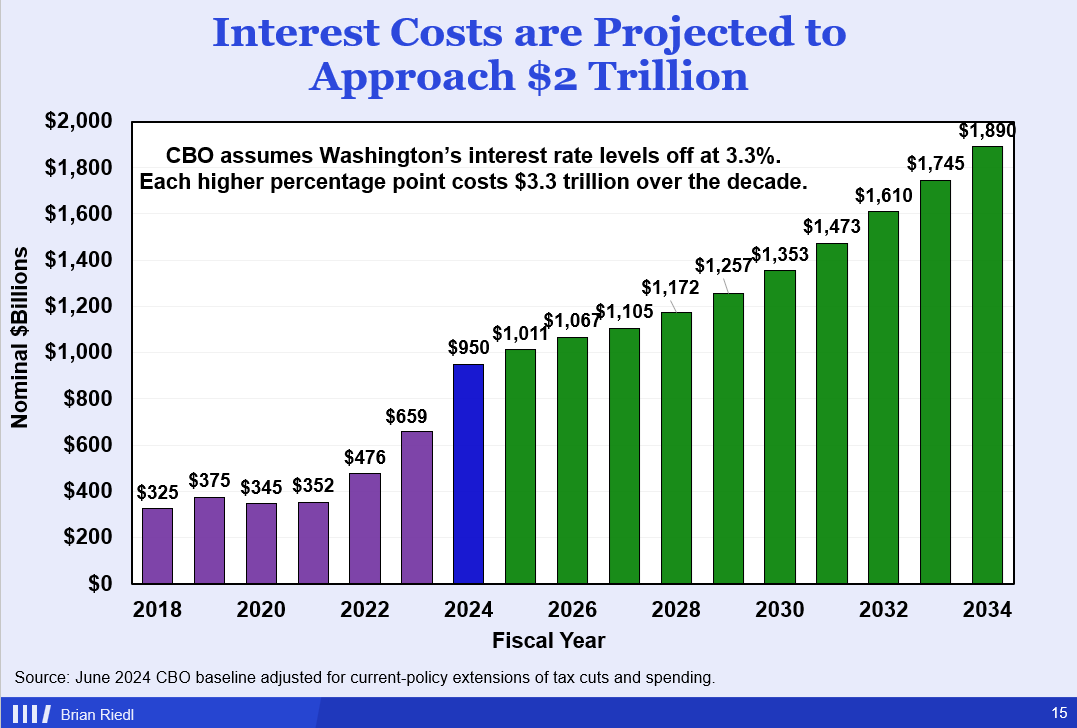

A big share of that increase in outlays comes from net interest on the public debt, which went up by $240 billion, or 34 percent in a year. Net outlays for interest on the public debt totaled $950 billion in 2024. This is just the beginning. Brian Riedl has a chart:

These projections are based on possibly too optimistic interest-rate levels. As Rauh reminds us, given “the historical volatility of interest rates and the challenges with economic forecasting, there are considerable risks to the forecast.”

He then goes on to look at what would happen

if over the coming decade interest rates were slightly higher each year, cumulating in a 1.0% rate difference in 2034. That is, instead of ending the next 10 years exactly where we’re starting, at less than 3.4% as the CBO forecasts, what if the average interest rate the federal government paid on its debt crept up to just 4.4%?

Check out Rauh’s projections.

Interest-to-Revenue Ratios

Year Rates I/Rev I/Rev*

2024 Baseline 18.2% 25.1%

2025 Baseline 20.2% 27.9%

2034 Baseline 22.9% 31.1%

2034 Plus 1% 29.7% 40.4%

2054 Baseline 34.8% 45.7%

2054 Plus 3% 62.3% 81.9%

Rev* excludes SS OASDI

payroll tax revenuesIt’s scary. Yet none of the candidates on the campaign trail seem to care much about that.

Politicians would rather talk about anything but our fiscal problems. They may even believe that it’s okay because we have a lot of time to fix whatever needs fixing. But if the rise of interest payments in the last four years tells you anything, it should be that we likely have less time than we think.